Staking or SEC? NFT Developers Face a Dilemma as FTX Launches New Marketplace

As NFTs on Solana enter a bear market, developers turn to passive income as a way of attracting new investors, but little do they know that their ‘solution’ causes even more problems.

The same story plays out each time a new crypto market emerges. Early adopters with strong convictions spend months building an empire, and after enough time passes, the often laughed at niche segment turns into an economic mammoth that attracts both the rich and the poor. Everyone joins and welcomes it as the next big thing, but by the time a bandwagon is formed, the market becomes oversaturated.

This is the story of Solana’s NFT ecosystem.

A brief history

The Proof-of-History blockchain network solved issues that Ethereum will not fix for at least a year until ETH2 comes out.

During an average Ethereum NFT mint (that is usually sold out in the span of minutes) investors face the following problems:

- Ridiculous transaction fees (anywhere from $50 to $1000)

- Transactions that randomly fail (if demand is high enough, users may miss the mint because of this)

- Slow transaction speeds (incentivizes minters to pay more gas to mint a token on time)

Resolving these issues is critical for the eventual massive adoption of non-fungible tokens, and we can’t afford to waste time — we need a better blockchain network for NFTs right now.

Lower fees and faster transaction throughput are what brought investors of all sizes to Solana. Being new, the network offered a significantly lowered entry level for developers and investors alike.

Those desiring a Crypto Punk suddenly had the option to purchase one for only a few hundred dollars, albeit a different version. Not to mention, investors could buy an NFT for 1 SOL and sell it for 100 SOL in the blink of an eye since Solana’s NFT market expanded incredibly fast early on.

A 100X profit with no liquidation and minimal downside. Sounds like a dream, right?

It all began with Solpunks. Then came Degen Ape Academy, Thugbirdz, Aurory, Frakt, Galactic Geckos, and so on. The investment thesis was to invest in good art, and beyond that, in a good, strong community. But as more projects launched on marketplaces like Solanart, the thesis reached a bottleneck.

The demand was there, but when spread over hundreds of projects that have nothing to offer beyond JPEGs, its power dissipated.

Greed also played a crucial part in turning Solana’s NFT supermarket upside down.

Collectors were not satisfied with scoring a +3000% investment. They wanted to sell their existing ‘bluechip’ NFTs to mint new projects in hopes of replicating their success and earning even more money.

Sure, an NFT that went from a 2 SOL price floor to 50 SOL could grow up to 200 SOL with enough time, but these users (referred to as ‘flippers’ by the community) were not that patient. They were more interested in testing their luck with new mints.

The problem here is that flippers created such enormous selling pressure transferring their capital to new mints that bluechips lost up to 50% of their value, which gave the impression that their growth was not sustainable. For comparison, imagine that everyone suddenly sold Bitcoin to buy altcoins. This would make Bitcoin appear weak and so the entire crypto market as well — which is what happened to Solana’s NFTs.

At the same time, another group of users saw the success that NFTs had and realized that they were an easy cash grab for creators. The average project sold a 10,000 token collection at a 2 SOL mint price — that’s roughly $3 million at current market prices! With that in mind, it’s no wonder that the market went haywire. We went from having 5 new collections a week to 10 a day. All it takes to launch a low-effort NFT collection is to pay an artist a few thousand dollars to create poorly-drawn JPEGs, so the rate at which new collections launch is no mystery.

To conclude, even though demand stayed the same (and potentially weakened due to the fact that blue chips lost a bunch of value), the supply did not.

The market became saturated with terrible projects that had nothing to offer beyond plain JPEGs that served as Twitter profile pictures, and flippers who once earned insane returns now began losing money as new collections had their floor price go below mint prices.

What happened then? Enthusiasm for NFTs had come to a halt, and so did volume inflows. The expansive segment did not keep up with its past growth, and the once bullish community turned bearish overnight.

In the midst of ever-growing frustration, developers were forced to adapt to changing market conditions in order to avoid extinction. They had to stand out in an oversaturated market, and so was born the idea of revenue-sharing mechanisms like staking.

Distributing Royalties

SOL NFTs are not the first to come up with the idea of rewarding community members to garner interest and incentivize long-term holding.

The first project to venture down that road is a social club and PFP avatar platform known as CyberKongz.

Holding one of their 1000 pixel apes grants the owner daily rewards. Everyone that holds onto their ape earns 10 BANANA tokens a day.

These tokens can be redeemed inside the CyberKongz ecosystem to claim new NFTs, unique names, and biographies. But they can also be exchanged for WETH on one of SushiSwap’s liquidity pools. At one point, the market valued BANANA tokens at $100 a piece. Yes, one hundred American dollars.

Token distribution is not yet common outside Ethereum NFTs. However, we now see a sudden rise in the adoption of such reward systems.

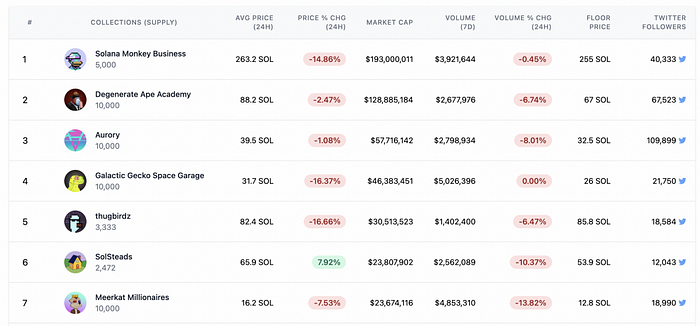

For example, Solana Monkey Business rewards owners with marketplace revenue. In this case, users owning a set of 4 NFTs earn daily rewards of up to $2,000.

As of recently, a number of developers have decided to adopt similar revenue models. To name a few:

- Meerkat Millionaires (100%)

- TurtlesNFT (70%)

- SolSnatchers (50%)

- FancyFrenchNFT (50%)

- PiggySolGang (30%)

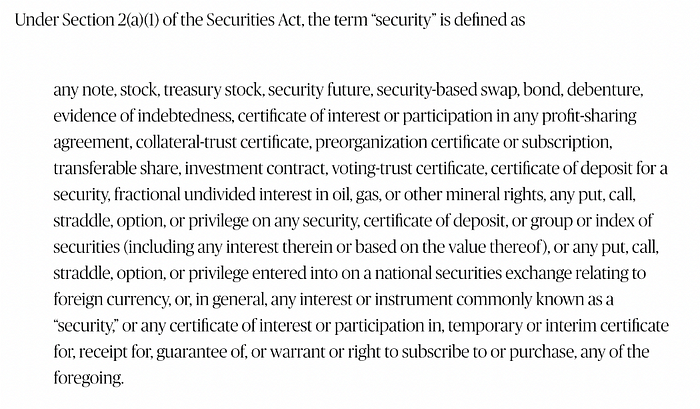

Note: the numbers above represent the % amount of total secondary sales (royalties) that each project distributes to its holders.The problem with distributing royalty revenue to holders is that it attracts bad attention. Under U.S. laws, the SEC is free to classify such tokens as securities.

Sidenote: Let’s be honest; most cryptocurrencies can be classified as securities. But teams that are in the NFT space for the long haul will not risk having their project torn apart by the SEC at some random point in the future. Even though regulators do not currently view NFTs as securities, they may and can do so later on. NFTs that reward holders with royalties are securities, and that’s a fundamental problem that developers must face head-on before it’s too late.

Despite their astonishing popularity, Chairman Gary Gensler has not issued any comments on the practice of issuing dividends within the NFT ecosystem. But that does not mean that platforms that facilitate their trading, like marketplaces, feel safe enough to let their guard down.

OpenSea’s NFT Crackdown

As mentioned earlier, developers had to innovate to survive. And after only one bearish week in Solana, many of them have moved forward with launching these various revenue systems.

Investors were full of joy upon hearing that their NFT of choice had decided to distribute royalties. Who wouldn’t be? After all, look at the rewards!

But the days of copious enthusiasm were cut short after an unexpected move made by no one other than OpenSea.

The Ethereum-based NFT auction house froze DAO_Turtles’ collection, which had previously announced staking rewards.

An email between the two teams revealed that DAO_Turtles violated OpenSea’s terms of service in respect to listing securities that award DeFi Yield bonuses, staking bonuses, and burn discounts.

Their decision became a turning point in the entire NFT ecosystem. Existing projects like CyberKongz, Mutantcats, BearsDeluxe, and ZombieToadz were now at risk of being delisted. No one took it lightly as OpenSea practically holds a monopoly over Ethereum’ NFT trading.

This wasn’t an isolated problem. The long-anticipated FTX NFT market was soon to launch, and the act of issuing monetary rewards became a burning question over at Solana’s NFT land. Is FTX also worried that the SEC may pressure them to close their market at some point?

It didn’t take too long to find out the answer.

Meerkats drama

The drama that unfolded between FTX and Solana NFTs began with cartoon pictures of meerkats.

Meerkat Millionaires Country Club (MMCC) is a collection of 9,999 NFTs that distributes its royalties to the community. What’s special about it? The team distributes 100% of its royalties. Yes, all fees gained from sales go back to the community; none go back to the team.

Other teams opt for only 30–50% revenue share, so it’s not surprising to see that MMCC is so popular that it consistently ranks second place on Solanart.

There’s strong demand for Meerkats. Everyone wants to be part of this cash machine, no matter how dubious their long-term sustainability is.

So when news of Opensea’s clash with DAOTurtles broke out, meerkat holders were worried whether the drama would spill over to Solana. And if it does, will FTX refrain from listing NFT collections with revenue models?

FTX US President Brett Harisson arrived at the forefront of this drama, or rather, he was there to explain the exchange’s stance on securities and NFTs.

In the midst of bearish market PA, collectors viewed FTX as a savior. A simple listing would drive new investors to sweep floors as most anticipated a positive outcome in respect to retail gaining the ability to buy NFTs with credit cards.

However, those who simultaneously rooted for royalties now realized that both outcomes are mutually exclusive.

Developers have a difficult choice in front of them: either launch staking or give up and opt for an FTX listing instead. Naturally, this caused great unhappiness in the community.

FTX isn’t really the boogeyman here. They’re a leading exchange that is forced to listen to regulators. They can’t risk their entire business because an objectively insignificant percent of their user base is unsatisfied.

Collectors initially held a grudge on FTX, but they soon realized the man with arms tied behind his back shouldn’t be the one to blame. Projects like TurtlesNFT have even happily obliged and reassured their community that abandoning staking is a better solution for the long term.

The ‘drama’ eventually boiled down to infighting between NFT projects themselves.

On the one hand, we have the Piggy Sol Gang, whose community supports staking in favor of decentralization, claiming that crypto investors abandon their core values by bowing down to regulatory agencies that don’t even cover the entire world.

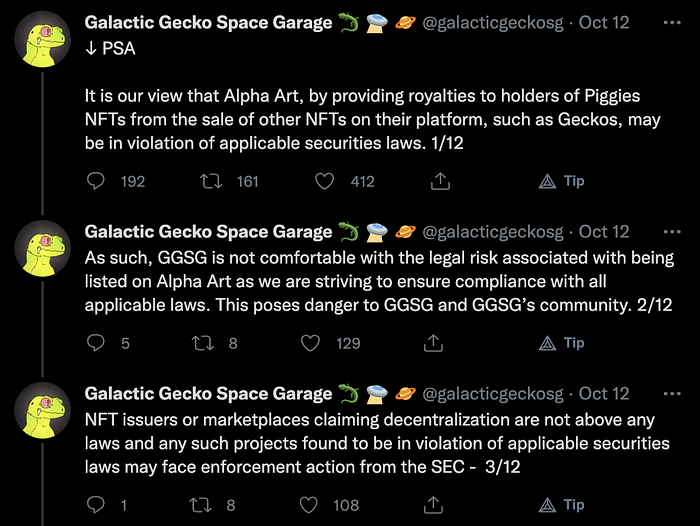

On the other hand, we have the Galactic Gecko Space Garage. This project went as far as to lawyer up in order to find a way to overcome regulatory hurdles. Their community ended up on the opposite end of the spectrum, claiming that the NFT community must concede and maturely come to terms with the fact that staking ultimately hurts developers and investors alike.

As you can see, the infighting brought up the question of decentralization vs. centralization. Any true crypto believer favors the former, but we can’t deny that the other side doesn’t have strong arguments.

Is anyone right? Both sides utter half-truths, and it almost seems as if the environment we’re presently in at this point in time does not offer any answers.

What Now?

This is sadly the end of the story. We haven’t reached any conclusion as the chain of events in the so-called metaverse continues to unfold. Truth be told, no real progress has been made at this point, we’re at a standstill. Moreover, it’s still too early to tell where the NFT ecosystem is headed as no new solutions have been offered by neither developers nor regulators.

So, what now?

As implied by FTX on numerous occasions, NFTs that distribute royalties can still earn a free listing. Brett Harisson offered consultation to developers in regards to customizing existing staking models, stating that teams do not have to completely let go of staking. Instead, they should edit their models so that they conform to U.S. securities laws.

This essentially means that projects can’t distribute SOL directly to holders as previously planned. The most likely alternative is to airdrop NFTs from a new collection as a way of rewarding holders that refuse to list tokens. Whatever it may be, all that developers must avoid is giving away monetary rewards in return for HODLing.

For a niche sector with a market cap of only $800 million, it is certainly weird to see so many hurdles early on. In previous bull markets, novel systems like ICOs were not regulated or hunted down for years. Is it because NFTs provide more insane, faster, and easier returns than all of their predecessors combined?

Only time can tell…or the SEC.

About us

Shrimpy is an automated portfolio management platform that helps cryptocurrency investors manage their capital through the use of a simple and intuitive app that saves time and money with the power of automation.

To find out more about our platform and discover how it can jumpstart your crypto journey, feel free to visit our main website.

We also provide free blockchain education to the masses at the Shrimpy Academy and Youtube.